Your bank statement doesn’t lie.

You can say that family matters most, but if you haven’t visited them in two years because you’re “saving money,” your spending tells a different story.

You can say creativity is important, but if you won’t buy supplies because they feel like a “luxury,” your budget reveals what you really believe: that your creative life is optional.

You can say you value growth, but if you won’t invest in therapy, coaching, or learning because it feels “irresponsible,” your financial decisions are speaking louder than your words.

Money is a mirror. And most of us don’t like what it shows us.

Not because we’re bad with money. But because the gap between what we say we value and where our money actually goes reveals uncomfortable truths about fear, scarcity, and the stories we’ve internalized about what’s “responsible.”

The Scarcity Lens

For many of us, money decisions are driven by a persistent whisper: There isn’t enough. There won’t be enough.

Even when objectively, there usually is.

This scarcity mindset shows up in ways we don’t always recognize:

- Staying in a draining job because leaving feels too risky

- Living like you’re broke even when your circumstances have improved

- Avoiding experiences you want because spending money on joy feels frivolous

- Saying no to opportunities that would stretch you financially—even when you could make it work

The fear of “not enough” becomes a self-fulfilling prophecy. You make decisions based on scarcity, and those decisions keep you feeling scarce.

Money and Identity

Financial stress isn’t just about the numbers. It’s tangled up with self-worth, belonging, and identity.

People avoid hosting friends because they’re not sure how their financial status compares to others.

They turn down professional opportunities because they’re worried about not fitting in with “more successful” people.

They stay small—in their careers, their social lives, their ambitions—because they’ve internalized the belief that money (or lack of it) defines their value.

Ramit Sethi, in I Will Teach You to Be Rich, talks about how guilt and shame around money keep people stuck. We tell ourselves we “should” be better with money, we “shouldn’t” spend on certain things, we “can’t afford” what we actually need.

And Brené Brown’s work on shame in Daring Greatly reinforces this: when we tie our worth to financial success or status, we stop making values-aligned decisions. We make fear-based ones.

The Shift: From Luxury to Necessity

One of the most powerful reframes around money is this:

Spending on what matters to you isn’t a luxury. It’s a necessity.

If creativity fuels you, art supplies aren’t frivolous—they’re essential.

If connection restores you, visiting family and friends isn’t extravagant—it’s foundational.

If growth sustains you, investing in therapy, coaching, or learning isn’t irresponsible—it’s strategic.

When you start viewing values-aligned spending as necessary rather than optional, your relationship with money changes.

You stop feeling guilty for prioritizing what actually matters. You start asking better questions: Is this expense aligned with my values? Does this purchase move me toward the life I want, or keep me stuck in scarcity?

Building Financial Courage in Small Doses

If scarcity has been your default for a long time, shifting to values-based spending can feel terrifying.

You don’t have to overhaul everything at once. You can build tolerance for financial risk the same way you build any muscle: in small, manageable doses.

Examples of dabbling:

- Opening an investment account with a small amount to learn how it works

- Buying a CD or exploring other financial tools to reduce intimidation through understanding

- Spending on something that feels like a stretch—and proving to yourself you can handle it

- Starting a side project or business while keeping your main job for security

- Investing in one meaningful experience (a trip, a course, a creative project) and seeing what shifts

The goal isn’t recklessness. It’s intentionality.

Taking calculated risks that align with what you actually want—rather than staying frozen in fear of “not enough.”

When the Spreadsheet Becomes Possibility

For some people, financial stress triggers avoidance. They don’t want to look at the numbers because seeing them feels overwhelming.

For others, making a plan creates calm.

When anxiety around money kicks in, a simple budget spreadsheet can be a powerful tool—not because you’ll follow it rigidly, but because creating it gives you a sense of control.

A spreadsheet that outlines:

- Current income and expenses

- Cash flow (where money is coming from and when)

- Assets and net worth

- Upcoming expenses and how to plan for them

The act of making the plan—even if you don’t follow it exactly—helps you see that success is possible. That you have options. That you’re not as stuck as it feels.

It’s the same principle as time management: planning when you’re stressed helps you focus and make progress, even if the plan changes along the way.

For Leaders: The Assumptions You’re Making

If you manage a team, you’re making financial assumptions about your people whether you realize it or not.

And those assumptions can create real harm.

Example: Business travel expenses.

If your company’s payment doesn’t go through for a hotel, one employee might cover it without blinking and wait for reimbursement.

For another employee, that same expense could put them in a precarious financial situation—maxing out a credit card, overdrawing an account, or creating stress they can’t afford.

But most people don’t want to tell their boss about their personal financial constraints. So they absorb the stress silently, or they start avoiding travel opportunities altogether.

Other ways financial assumptions create friction:

- Expecting everyone to have the flexibility to take unpaid time off

- Assuming people can afford to relocate for a promotion without relocation support

- Scheduling team events or professional development opportunities that require personal expense

- Not addressing cost-of-living increases while expecting loyalty and high performance

Even people in the same role may have vastly different financial realities. Student loans. Family obligations. Medical expenses. Housing costs.

What helps:

- Don’t assume financial flexibility. Ask what support people need.

- Make reimbursements fast and frictionless.

- Offer stipends or budget flexibility for professional development, not just “opportunities”

- Address compensation equity and cost-of-living openly

- Create psychological safety around financial conversations so people can advocate for themselves without shame

When leaders ignore financial stress, they lose good people—not because those people aren’t capable, but because they can’t afford to stay.

The Tool: Values-Based Budget Reflection

This isn’t about creating a perfect budget or tracking every dollar. It’s about examining whether your financial decisions reflect what you say matters most.

Step 1: Identify Your Core Values

Choose 3-5 values that matter most to you right now. Examples:

- Health/Wellbeing (therapy, movement, rest, nutrition)

- Growth/Learning (courses, books, coaching, skill-building)

- Connection (travel to see loved ones, hosting, quality time)

- Security (emergency fund, insurance, retirement, stability)

- Freedom (debt payoff, flexible work, time autonomy)

- Creativity/Joy (hobbies, experiences, beauty, play)

Step 2: Review Where Your Money Actually Goes

Look at the past 3 months of spending. Group expenses into categories that align (or don’t) with your values.

Questions to ask:

- What percentage of my spending goes toward my stated values?

- Where is money going that doesn’t align with what I say matters?

- What am I calling a “luxury” that’s actually essential to my wellbeing?

- What “necessary” expenses are really just old rules I haven’t updated?

Step 3: Examine the Trade-Offs

For any spending that doesn’t align with your values, ask:

- Was this necessary at one point? (Maybe it was—but is it still?)

- What am I trading for this expense? (Time? Energy? Opportunity? Peace of mind?)

- If my circumstances have changed, have my spending patterns caught up?

Sometimes we keep living like we’re broke long after our situation has improved. Sometimes we’re spending on things we don’t actually care about because we haven’t stopped to question the habit.

Step 4: Make One Intentional Shift

You don’t have to overhaul everything.

Choose one small change that brings your spending closer to your values:

- Cancel a subscription you don’t use and redirect that money toward something that matters

- Budget for one meaningful experience this quarter

- Invest in something you’ve been calling a luxury (therapy, a course, creative supplies)

- Build an emergency fund so “unexpected” expenses stop derailing you

- Allow yourself to spend on connection without guilt

The goal: Align money with meaning. Not perfection—just progress.

Closing Thoughts

Money reveals what we actually prioritize—not what we wish we prioritized.

And that gap—between what we say and where our money goes—is often where the most important growth happens.

If scarcity has been your lens for a long time, it’s understandable. Financial stress is real. Survival mode is real.

But at some point, you have to ask: Am I still making decisions based on old constraints that no longer apply?

You’re allowed to update your financial rules.

You’re allowed to spend on what matters to you without guilt.

You’re allowed to invest in growth, connection, creativity, and joy—not someday when you “have enough,” but now, because these things are what make life worth living.

Your bank statement is a mirror. What does it show you?

And more importantly—what do you want it to reflect?

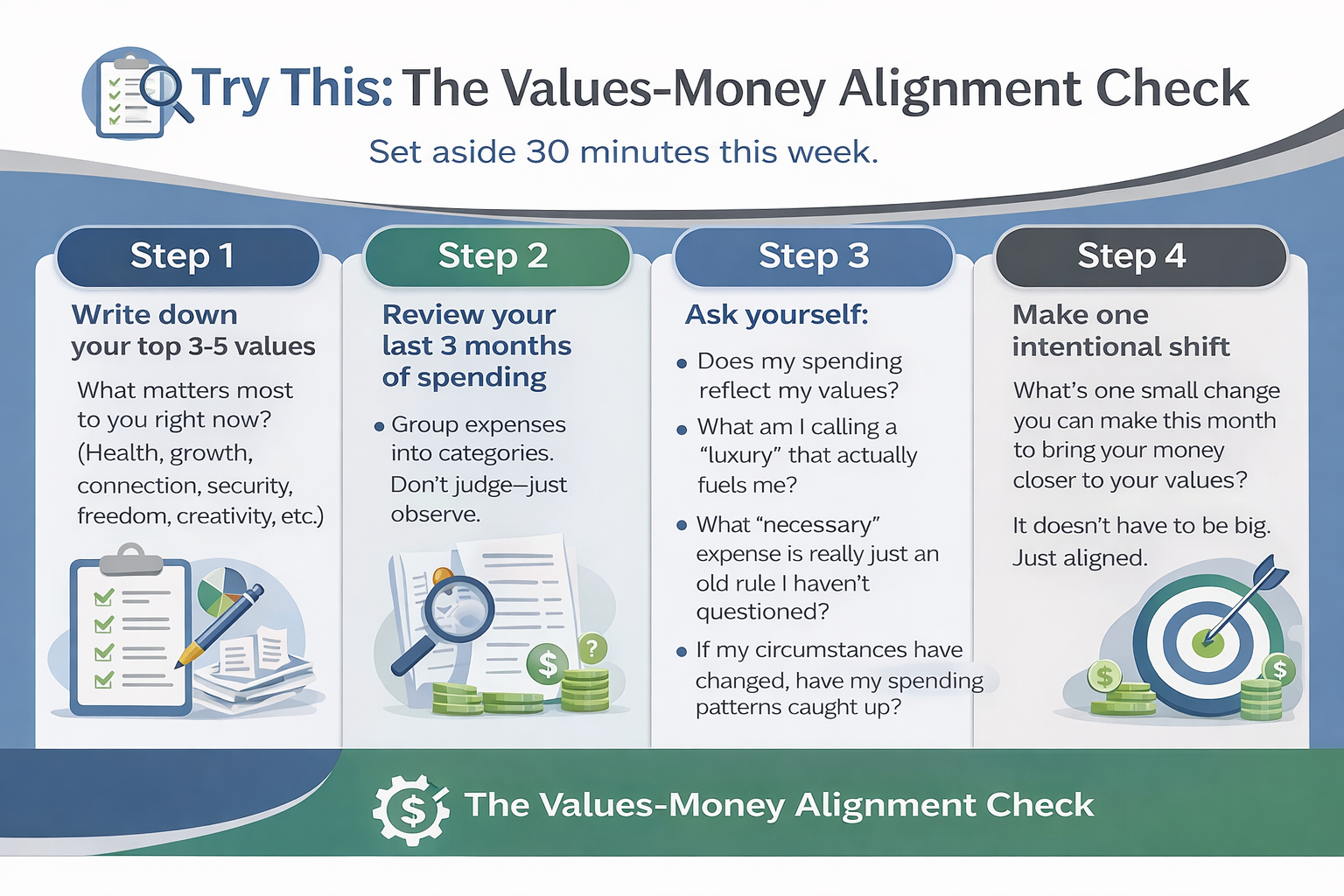

Try This: The Values-Money Alignment Check

Set aside 30 minutes this week.

Step 1: Write down your top 3-5 values.

What matters most to you right now? (Health, growth, connection, security, freedom, creativity, etc.)

Step 2: Review your last 3 months of spending.

Group expenses into categories. Don’t judge—just observe.

Step 3: Ask yourself:

- Does my spending reflect my values?

- What am I calling a “luxury” that actually fuels me?

- What “necessary” expense is really just an old rule I haven’t questioned?

- If my circumstances have changed, have my spending patterns caught up?

Step 4: Make one intentional shift.

What’s one small change you can make this month to bring your money closer to your values?

It doesn’t have to be big. Just aligned.

References:

- Sethi, R. (2019). I Will Teach You to Be Rich: No Guilt. No Excuses. No BS. Just a 6-Week Program That Works. Workman Publishing.

- Brown, B. (2012). Daring Greatly: How the Courage to Be Vulnerable Transforms the Way We Live, Love, Parent, and Lead. Gotham Books.

- Twist, L., & Barker, T. (2017). The Soul of Money: Transforming Your Relationship with Money and Life. W. W. Norton & Company.

If you’re navigating financial stress that’s tangled up with identity, values, or career decisions, I’d be honored to help. Schedule a free discovery session and let’s talk about what alignment between your money and your values could look like.